Ever wondered how professional gamblers and investors decide how much to risk on a single bet or investment? The Kelly Criterion is a mathematical approach that helps you decide stake size when you believe you have an edge, whether in markets or on a sporting market.

It is not a magic trick or a guarantee of profit. Think of it as a method for balancing potential gains against the risk of loss, helping you manage money more deliberately.

If you want to understand how it works and whether it might fit your approach, read on and you will find clear explanations and an example to make the concept practical.

What Is the Kelly Criterion Formula?

The Kelly Criterion is a formula for choosing what fraction of your bankroll to risk on an opportunity where you believe the offered return exceeds the true probability of success. It focuses on stake sizing rather than picking winners.

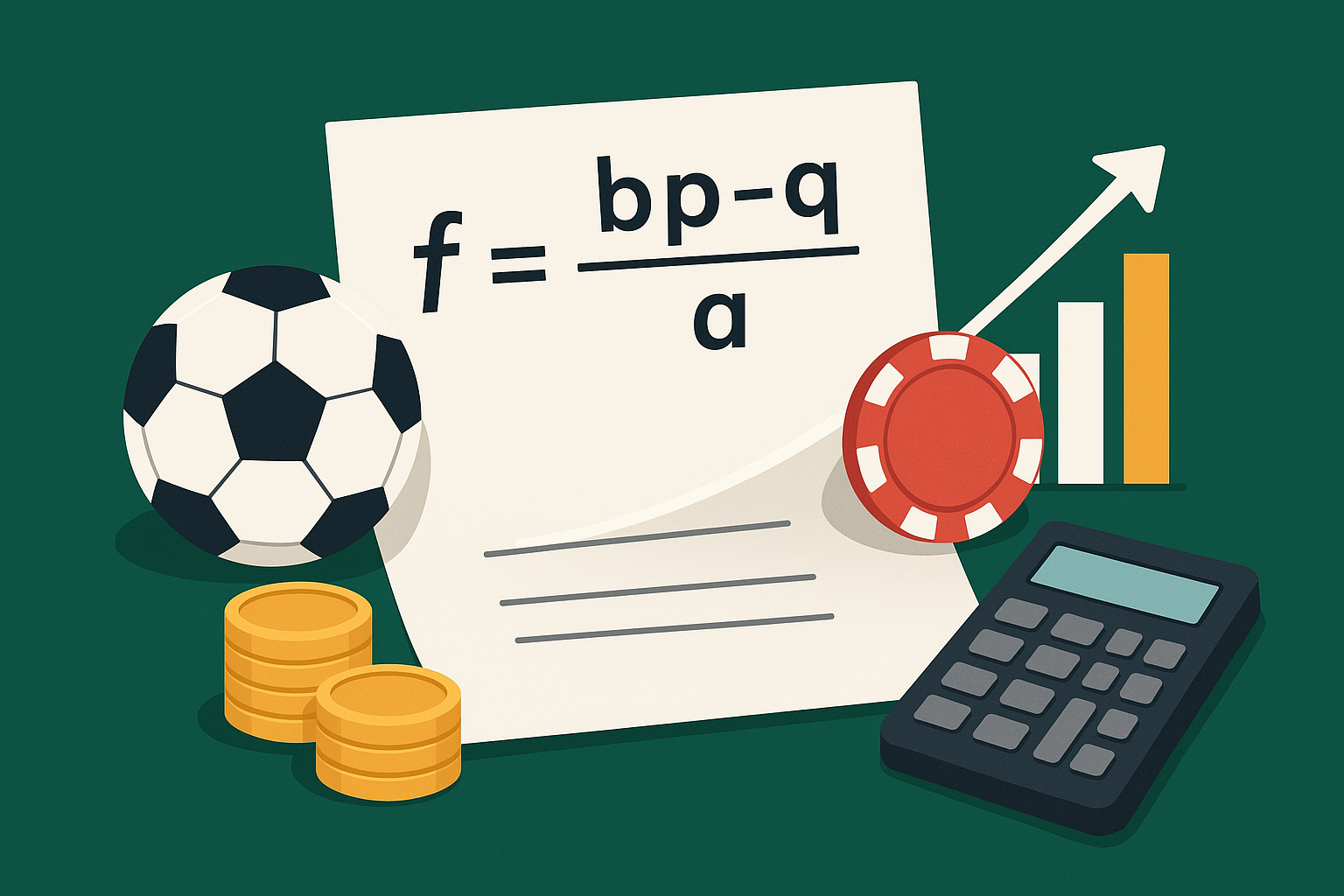

In plain terms, the formula uses three inputs: the odds being offered, the probability you assign to the outcome, and the complement of that probability. Written for decimal odds, the core expression is:

Kelly % = (b p − q) / b

Here b is the odds minus 1 (so decimal odds 3.00 gives b = 2), p is your estimated probability of success, and q is 1 − p, the chance of losing. The result is a fraction of your bankroll you might stake.

The criterion aims to maximise growth of capital over many repeated opportunities, while limiting the risk of ruin by reducing stake size when the perceived edge is small or negative.

How Does the Kelly Criterion Work in Betting?

When applied to betting, the Kelly Criterion translates a perceived advantage into a recommended stake. If your estimate of the chance of winning exceeds the implied probability in the odds, the formula produces a positive fraction and suggests risking part of the bankroll. If there is no edge, it recommends staking zero.

Two practical points are important. First, the outcome depends entirely on the accuracy of your probability estimate. Second, the formula can indicate large stakes when your estimated edge is big, which may exceed your personal comfort with risk. Many users therefore apply a fractional Kelly, staking a portion of the Kelly result to reduce volatility.

Used thoughtfully, the approach encourages measured staking based on a consistent method rather than emotional reactions. Keep personal limits and financial wellbeing in mind when interpreting the formula’s output.

How Is the Kelly Criterion Applied to Investing?

In investing, the principle is similar: it helps determine position size in a trade or investment where you have an estimate of the expected return and the probability of success. The Kelly idea can be adapted to portfolios by treating each position as an investment with an edge and sizing positions to balance expected growth and drawdown risk.

Practically, investors often adjust the pure Kelly recommendation to reflect uncertainty in their estimates, diversification needs, and liquidity constraints. For example, an investor may use a fractional Kelly to reduce concentration risk, or limit position sizes to a small percentage of total assets to preserve diversification.

The criterion is a tool for position sizing, not a model for forecasting markets. It can complement other risk-management practices such as stop-loss policies, allocation limits, and periodic rebalancing.

Why Does the Kelly Criterion Matter for Long-Term Growth?

The reason the Kelly Criterion attracts attention is its theoretical focus on maximising long-run growth of capital while avoiding catastrophic loss. By converting an advantage into a mathematically derived stake, it attempts to maximise geometric growth rather than short-term returns.

That focus produces behaviours that differ from naive staking. For instance, it reduces stakes when the edge is small, avoiding overexposure, and increases stakes when the edge is clear, so capital compounds faster over repeated favourable opportunities. In practice, many practitioners prefer a tempered version because the full Kelly can lead to sharp swings in capital.

Understanding this trade-off between growth and volatility helps you decide whether the Kelly approach fits your goals and temperament. It is best seen as part of a disciplined plan rather than a guarantee of success.

Common Misconceptions About the Kelly Criterion

A frequent misconception is that the Kelly Criterion guarantees profit or removes risk. It does not. Its output is only as good as the inputs, and it cannot compensate for poor probability estimates or changing market dynamics.

Another misunderstanding is that Kelly eliminates the need for judgement. In reality, accurate probability assessment and sensible handling of uncertainty remain essential. Overconfidence in estimates can produce worse outcomes than simpler staking rules.

Finally, some assume Kelly always prescribes aggressive bets. In fact, it may recommend no bet at all when there is no edge, and many users deliberately scale the recommendation down to match their risk tolerance.

How Do You Calculate Optimal Bet Size Using the Kelly Criterion?

The calculation can be demonstrated with a concrete example to make the algebra clear and to show how the result becomes a practical stake size. This narrative example uses a single hypothetical opportunity to illustrate the mechanics.

Suppose a bettor has a £100 bankroll and sees decimal odds of 3.00 on an outcome that they estimate has a 50 percent chance of happening. In the formula, b equals 2 (3.00 minus 1), p equals 0.5, and q equals 0.5. Plugging these into the Kelly expression, the calculation works out as follows, producing a fraction of the bankroll to stake. The arithmetic gives 0.25, meaning 25 percent of the bankroll; in this case that would be £25.

This numerical example shows how the formula converts your probability estimate and the market’s odds into a stake recommendation. It also highlights why accuracy matters: a small change in your probability estimate can materially change the suggested stake. Many practitioners therefore use a fraction of the computed Kelly percentage to account for estimation error and to reduce variance.

Limitations and Considerations of the Kelly Criterion

There are several practical limitations to bear in mind. The Kelly Criterion assumes you can estimate the true probability of success, which is difficult in many real-world situations. Errors in these estimates will lead to inappropriate stake sizes.

The approach also does not automatically account for real-life constraints such as liquidity, trading costs, bet size limits, or the need to keep assets diversified. Pure Kelly can produce concentrated positions and volatile equity paths, so many users prefer scaled versions or integrate Kelly with other risk controls.

Personal circumstances matter too. Your financial goals, time horizon, and psychological tolerance for drawdowns should shape how strictly you follow any mathematical staking rule. Use the criterion as one input among many in a prudent risk-management framework.

Should You Use the Kelly Criterion for Your Financial Decisions?

Deciding whether to adopt the Kelly approach depends on how confident you are in your probability estimates and how much volatility you can accept. If you have a robust method for estimating edges and can tolerate variance, Kelly or a fractional Kelly can be a disciplined way to size positions. If your estimates are uncertain or you value steadier short-term returns, a more conservative approach may be appropriate.

Whatever you choose, treat the Kelly Criterion as a tool that informs decisions rather than as an automatic prescription. Combine it with clear allocation rules, sensible limits, and periodic review of assumptions. If you would like, we can show how a fractional Kelly would change the example above or model different probability scenarios to see their impact.

Use tools and limits to protect your finances, and make choices that suit your personal situation. The Kelly Criterion can help structure staking, but responsible decision making and preserving wellbeing always come first.

**The information provided in this blog is intended for educational purposes and should not be construed as betting advice or a guarantee of success. Always gamble responsibly.